AI and the Energy Transition: Synergy or Stress?

Will AI's growing energy demands accelerate or hinder the global energy transition away from hydrocarbons?

AI and the Energy Transition: A Geopolitical Nexus

AI and the energy transition are two secular themes that carry immense implications for global geopolitics. But the strategic value of AI may outweigh energy transition efforts.

These trends are not isolated. They are deeply interconnected, much like M.C. Escher’s Drawing Hands lithograph, where each hand creates the other.

The surge in AI demand is driving a significant increase in electricity consumption by data centers, many of which still depend heavily on fossil-fuel-powered grids.

Simultaneously, governments are implementing targeted industrial policies to secure their positions in the energy transition race and reduce reliance on hydrocarbons. The question remains: will AI slow these efforts down?

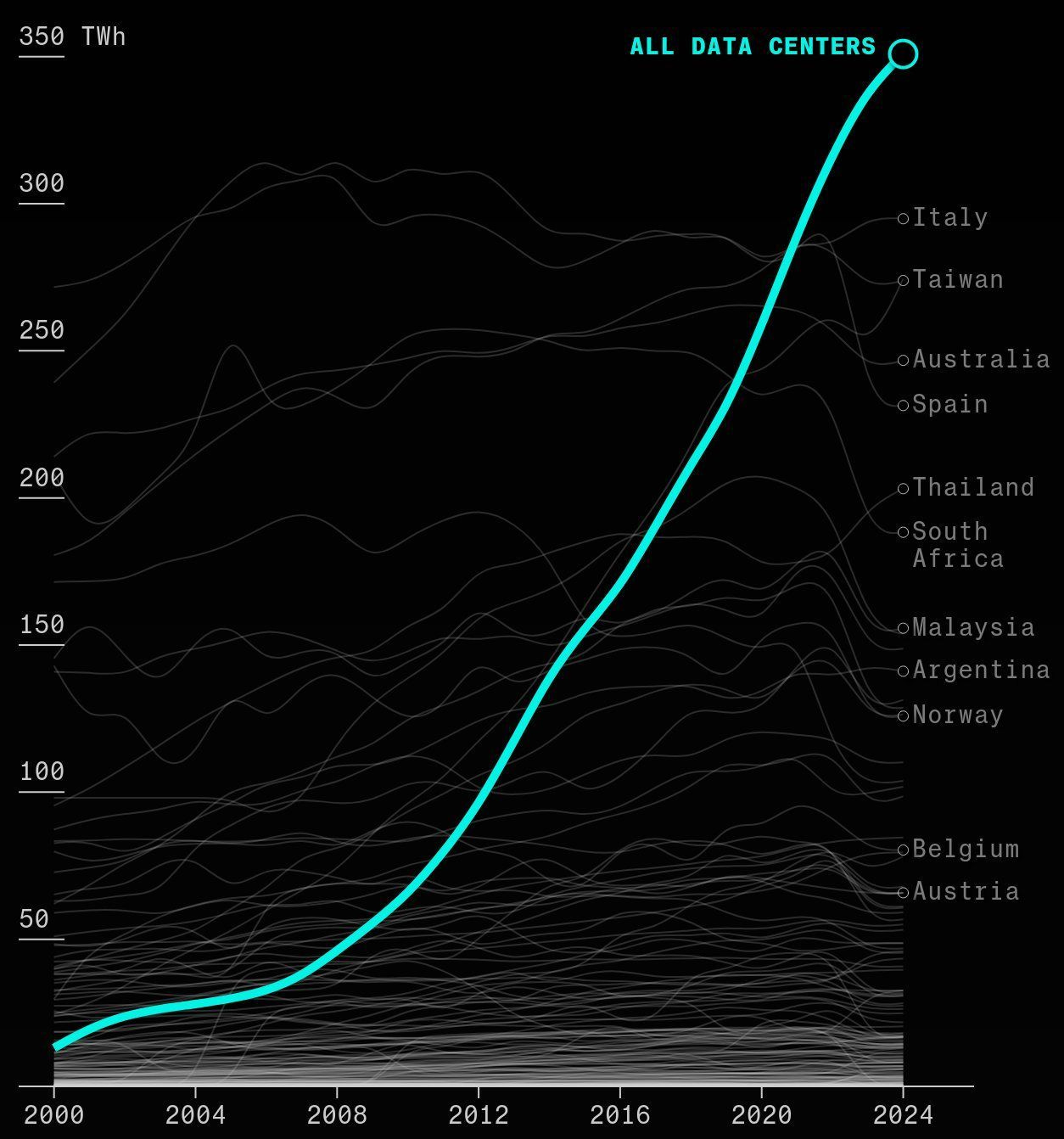

Data Centers, Power Consumption, & Energy Infrastructure

In Europe, projections indicate that by 2026, electricity use by data centers in the European Union will be 30% higher than in 2023 due to the rise in new facilities and increased AI-driven digitalization. Ireland, for instance, could see data centers accounting for nearly a third of its total electricity demand by 2026.

The primary energy consumers within data centers are cooling systems and servers, each responsible for around 40% of total consumption, with the remaining 20% used by power supply systems, storage, and communication equipment.

Currently, data centers are responsible for 1-2% of global electricity usage, a figure expected to increase to 3-4% by the end of the decade. AI's growing footprint could lead to it representing about 19% of data center power demand by 2028.

According to Goldman Sachs, the U.S. is expected to see data centers consuming 8% of its electricity by 2030, up from 3% in 2022. To meet this rising demand, U.S. utility companies need to invest approximately $50 billion in new generation capacity.

Additionally, this surge in consumption could require around 3.3 billion cubic feet per day of additional natural gas, necessitating the construction of new pipeline infrastructure. In other words, more investment in fossil fuels needed to power the surge in energy consumption from AI.

Globally, Europe houses roughly 15% of the world’s data centers. By 2030, the energy demand from these centers could equal the combined current consumption of Portugal, Greece, and the Netherlands.

Both the US and European energy grids have ~60% of their energy generated from fossil fuels which provide more consistent energy outputs and utilization rates. In contrast, renewables like wind and solar exhibit significantly lower utilization rates as a function of their intermittent and less dependable nature.

Consequently, as demand for AI grows for both economic and geopolitical applications, the necessity for consistent energy inputs rises at commensurate rate. As of now, fossil fuels are able to accomplish this far more effectively than renewables.

A Steep Cost & a Paradox

The computational power needed for training AI models is increasing rapidly, with costs doubling every nine months. This growing demand could lead to data centers consuming energy equivalent to that of entire states like Sweden or Germany by 2026.

According to Time Magazine, the environmental impact includes a significant rise in water usage: estimates are suggesting global AI demand might drive data centers to consume over a trillion gallons of fresh water by 2027.

Advancements in chip efficiency, like NVIDIA's new GPUs, which consume 25 times less energy than their predecessors, offer hope for reducing AI's energy footprint. However, Jevons Paradox suggests that as efficiency improves, overall usage may increase, thereby countering the benefits of these advancements.

The Nuclear Option?

Nuclear energy is increasingly seen as a vital part of the energy mix due to its ability to provide consistent, carbon-free baseload power. By 2025, global nuclear generation is expected to surpass previous records set in 2021, with growth driven by countries like France, Japan, China, India, Korea, and several in Europe.

In response to rising AI-related energy demands, companies like Amazon are investing in nuclear-powered data centers. Exempli gratia: AWS recently acquired a Pennsylvania-based nuclear facility to meet the power needs of its expanding AI operations.

Nuclear energy also offers significant land-use efficiency, requiring far less space than wind or solar farms, and has a longer operational life, typically between 40-60 years, compared to 20 years for wind farms and 30 years for solar.

Modular Reactors (SMRs) are poised to play a key role in the future of nuclear energy. Their smaller, modular design allows for greater flexibility in site selection and quicker, more cost-effective construction.

Prefabricated units can be manufactured and assembled on-site, making SMRs more adaptable to rising energy demands while offering the reliability and low-carbon benefits of traditional nuclear power.

Geopolitics of AI, Data Centers, Energy

According to Reuters: "The White House announced a new task force to deal with the growing needs of AI infrastructure after a meeting on Thursday between senior U.S. officials and top technology and power company executives."

The White House stated that the participants talked about addressing clean energy needs, permitting processes, and workforce demands essential for building data centers and power infrastructure to support advanced AI operations.

President Joe Biden's administration is urging tech companies to invest in new climate-friendly power generation to meet their growing demand. The increased demand from AI could make it harder for Biden to achieve his goal of decarbonizing the power sector by 2035 in the fight against climate change.

As I have previously written in past weekly insights, supply chains are being re-organized not for economic maximization, but geopolitical optimization. This is especially pronounced in two areas already mentioned above: advanced AI-interfacing semiconductors and the energy transition. And data centers sit at the crux of both.

The US-China rivalry in particular and efforts for reaching net zero emissions have triggered a race to secure strategic minerals that are essential to the economic and political security of both nations. As a result, countries are reforming global supply chains as emerging industries demand consistent access to these inputs.

Case in point:

Following Russia’s invasion of Ukraine, the US banned all imports of Russian uranium. However, the slavic behemoth supplies nearly 20% of the uranium used in U.S. nuclear reactors. Specifically, the US has limited domestic capacity for producing high-assay low-enriched uranium (HALEU).

At the time, this was filled by Russia's advanced enrichment capabilities. But with the ban, this poses a major issue for US-based SMRs which rely on HALEU for fuel. This dependency poses a significant challenge for energy security vis-a-vis data centers and the use of nuclear technology to power them.

More broadly, as geopolitical tensions strain these supply chains, deployment of SMRs in the US may encounter delays and cost overruns.

Consequently, the ban created a substantial gap that the U.S. must now fill through increased domestic production or sourcing uranium from other countries like Canada, Australia, or Kazakhstan.

The Central Asian country is the world's largest and cheapest uranium producer, thanks to its use of in situ leaching (ISL), a low-cost extraction method that allows uranium to be produced at around $10 to $35 per pound. The devaluation of the Kazakh tenge has also made its uranium exports even more competitive globally.

Washington is also now investigating whether China is bolstering Russia's nuclear industry by circumventing US sanctions and importing enriched uranium from Russia and then exporting its own production to the U.S. Re-direction through so-called middle countries is a new strategy Beijing has adopted to counter de-risking efforts.

In this high-stakes race, nations aren't just vying for dominance in AI—they're contending for control over the energy that will power the future. The question is: who will rise to the challenge and who will falter, leaving their mark not as innovators, but as those who let the future slip away?