Battle of the Bytes: Too Little Too Late for China in AI US Face-Off

China's retaliatory measures against US semiconductor measures could backfire and accelerate their rivals's place in the AI race

The Promethean War

The US and China continue to engage in their Promethean War for technological supremacy amid a broader struggle for greater hegemonic influence. The tech-for-tat exchanges are impacting global markets, and tensions are likely to escalate.

By most accounts and metrics, the US still pulls ahead of China when it comes to the sophistication of its semiconductors and AI-interfacing chips. Maintaining this lead is predicated on ensuring China does not achieve technological parity with the US.

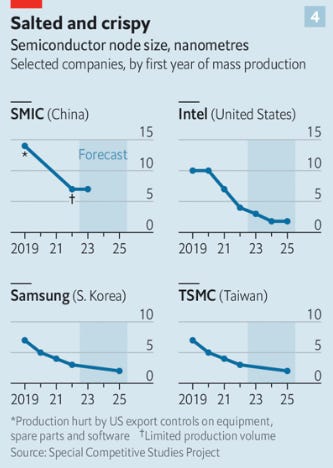

Source: The Economist

The US continues to act as an economic magnet, attracting the most talented workers and researchers into the industry relative to its Sino counterpart. At the same time, wilting relations between the two competing powers also means fewer cross-student exchanges.

Furthermore, the nature of China’s political economy and digital Great Firewall means it faces semi-structural obstacles to growing domestic generative AI capabilities and the hardware to power them.

AI-enabled technologies like ChatGPT are efficient and effective because they are trained on petabytes of unstructured data that’s been generated over time. In this regard, America has an advantage: 56% of all global websites are in English, with only 1.5% in Chinese. Consequently, the pool of available data from which large language models can learn from is considerably larger for the US than for China.

Furthermore, as The Economist correctly points out, “the Chinese interact with the internet primarily through mobile super-apps like WeChat and Weibo…These are “walled gardens…so much of their content is not indexed on search engines.”

But there is also the hardware element: In late 2022 the US and Western allies imposed a myriad restrictions on the export of certain technological components with the potential to enhance China's capabilities in the field of artificial intelligence.

These restrictions encompass the high-performance microprocessors utilized within cloud-computing data centers, which play a pivotal role in the training of foundational AI models like ChatGPT.

In summary, China is at disadvantage relative to the US because they lack:

❌The data pool necessary to make scaleable and competitive generative AI

❌Technological know-how to make cutting edge semiconductors

❌Insufficient talent for developing advanced software and hardware to power AI

A Pound of Flesh, But no Byte

In response to US and Western-allied restrictions of strategic technology to China, Beijing requested a consultation with the World Trade Organization (WTO). In other words, China formally initiated a dispute against the US’ measures, claiming it is:

“…inconsistent with multiple provisions of the WTO's General Agreement on Tariffs and Trade 1994, the Agreement on Trade-Related Investment Measures, the Agreement on Trade-Related Intellectual Property Rights, and the General Agreement on Trade in Services.”

The WTO’s response was:

“Issues of national security are political matters not susceptible to review or capable of resolution by WTO dispute settlement. Every Member of the WTO retains the authority to determine for itself those measures that it considers necessary to the protection of its essential security interests, as is reflected in the text of Article XXI of the GATT 1994, Article XIV bis of the GATS, and Article 73 of the TRIPS Agreement.”

In other words, if the policies are based on preserving national security, there is little the WTO can do. It is therefore no accident, that China used a similar justification to retaliate against the US…

Oh, So That’s How it is

Having said all this, China does have some leverage when it comes to the resources needed to make advanced and middle to low-end chips. The Asian giant has a virtual monopoly not on rare earth metals per se, but on processing and exporting them.

According to the IEEE, the three most metals used to make semiconductors are all primarily produced in China:

🇨🇳Silicon ➡ 64% of global production

🇨🇳Germanium ➡ 60% of global production

🇨🇳Gallium arsenide ➡ 80% of global production

In response to Washington restricting China’s access to high-end, AI-interfacing chips, Beijing has imposed new controls on access to germanium and gallium. Exporters in China will now have to fill out special licenses, but it is unclear how rigorous the permitting process will be.

This would not be the first time Beijing leveraged the behemoth of the state bureaucracy to impose artificial red tape as a political statement/geopolitical strategy. But as Agathe Demarais, author at Foreign Policy noted: “Weaponizing commodities is in fashion”. Look no further than the war in Ukraine and weaponization of Russian petroleum.

A study by the U.S. Geological Survey concluded that reducing a third of the supply of gallium to US firms would trim 2 percentage points from GDP forecasts. While this would present short-term pain, it would ultimately accelerate the US’ ABC policy: Anything But China.

Russia’s invasion of Ukraine is a prime example of geopolitical stress from an adversary accelerating decoupling efforts; the same dynamic would play out if China resorted to resource nationalism and weaponized its centrality in the supply chain.

As a matter of fact, China ironically would be making the same mistake the US has made countless times: imposing unilateral sanctions/restrictive economic measures and eroding confidence as a reliable trade partner and spurring alternative suppliers.

Swinging the sword of sanctions and unilateral economic measures has diminishing marginal returns: the more you use it, the duller the blade gets until all you’re left with is a butter knife. But for China, the situation would be worse. For one, unlike the US, China does have a reserve currency, and therefore lacks the same policy flexibility and has to be more careful in how they exercise power.

Additionally, a sudden rise in the prices of these weaponized resources would incentivize new producers to join a market with now comparatively more attractive profit margins. Coupled with growing allied efforts to create a Western mining bloc and tax incentivizes to spur additional competition, Chinese influence would wilt.