The Gordian Knot: Climate Policy vs Environmental Policy

The cost of one is the other, and arguments for a "sustainable" middle are too nebulous to take seriously - at least for now.

Under the current geopolitical and technological conditions, governments cannot demand both climate and environmental policy. But before we continue, it’s important to define terms:

Climate policy - Shifting away from fossil fuels and towards renewables as the primary source of energy.

Environmental policy - Preserving the integrity of biological ecosystems.

There is an inherent contradiction here. Indonesia’s rainforests have been razed to establish palm oil plantations aimed at biofuel production, and West African forests “are felled to supply wood pellets for heating Europe’s eco-conscious homes”.

Energy transition renewables require an immense amount of resources. For example: battery electric vehicles (BEVs) are typically 15 to 20 percent heavier than comparable internal-combustion engine (ICE) vehicles.

To produce an equivalent amount of electricity, photovoltaic (solar) power generation consumes 40 times more copper, and wind power requires up to 14 times more iron compared to fossil fuel-based power plants like coal or natural gas facilities.

Fossil fuel plants require less mineral input per unit of energy generated due to their simpler infrastructure and direct combustion process, which doesn’t rely on extensive cabling, conductive materials, or turbine systems needed in renewables.

The energy transition is riddled with cost factors beyond the appetite of private sector firms who also have to navigate a labyrinth of regulations. Most of which are now at the intersection of climate and environmental policies.

Policymakers are demanding both rhetorically and through legislation for companies to do both. But unless public sector support is given through subsidies, tax incentives, R&D, etc, the private sector in free-market economies won’t shoulder the costs without passing them onto consumers.

And then you end up with greenflation (“the increase in prices of materials, components, and energy due to the transition to renewable energy”). One country is the perfect exemplification of this dilemma: China.

Case in Point: China

In countries like China - where 40% of all firms are classified as state-owned enterprises (SOEs) - firms receive huge public sector support, but this is not sustainable - so to speak. The Asian giant is hardly the bastion of environmental conservation, yet you can argue they lead in climate policy.

In 2023, the Asian giant accounted for approximately 60% of total global BEV sales. Equally for solar panels, the sun shines bright on Beijing. In 2023, China installed 170 gigawatts (GW) of new solar capacity, which accounted for around 43% of the global total of approximately 400 GW.

Source

But this came at the cost of the environment. The Yangtze River is the world's largest source of ocean plastic; Beijing's particulate pollution is 40% higher than the most polluted county in the United States; and China is the largest global CO2 emitter, contributing nearly 31% of emissions in 2022.

And the Asian giant uses its staggering 1,161 coal-fired power plants—the most worldwide— to produce solar panels and EVs. Irony abounds.

Brazil: From Bossa Nova to Terra Nova

Renewable sources account for approximately 46% of Brazil's total energy supply, far above the global average, and over 93% of its electricity generation. In this regard, Brazil is leading in climate policy.

Environmentally, however, South America’s largest economy is falling behind. Approximately 17% of the Amazon rainforest has been deforested, with an additional 17% degraded by selective logging, fires, and land clearing. And the energy transition has not even fully taken off yet

Much of Brazil’s critical mineral bounty remains uncharted. Only a small fraction of the Amazon—less than 1%—has been explored comprehensively, leaving vast areas under the dense canopy effectively unknown in terms of mineral deposits.

What is known indicates that the Amazon likely holds significant quantities of strategic minerals. Brazil has substantial deposits of iron ore, manganese, bauxite, and gold, and smaller reserves of minerals like nickel, cobalt, lithium, and rare earth elements.

Much of the nation’s known bauxite and iron ore deposits, for example, are concentrated in the Carajás region of the eastern Amazon. This untapped potential positions Brazil at a pivotal point between economic opportunity and environmental stewardship—a tension that only intensifies as global demand for critical minerals outpaces supply.

As we saw during the 2000s commodity boom - driven by emerging-market growth, Chinese demand, and a weak U.S. dollar - Brazil may again find itself at the epicenter of a mineral rush.

Today’s dynamics, however, are steered not just by growth but by the geopolitical and technological race to secure resources for the energy transition. This context makes Brazil’s mineral wealth an asset of profound geoeconomic and political value.

No politician or strategist could afford to sideline these benefits. The likely outcome is that geopolitics will dictate a policy shift, where environmental ideals make room for strategic extraction.

This tension is deepened by Brazil’s reliance on mining, agriculture, and energy exports—industries likely to clash with President Luiz Inácio Lula da Silva’s environmental agenda.

But with its minerals, Brazil could diversify critical supply chains and capitalize on the de-risking from China trend. Offering an alternative supply chain would likely cultivate political capital vis-a-vis the United States.

In this framework, Brazil’s resources have the potential to transform not only its economy but its role in a redefined global order - even if that means reshaping environmental policy to meet geopolitical ends.

The Deciding Factor: Technology

Many opposed to the dilemma I outlined above will respond by saying that if the proper technologies were achieved at scale to facilitate mass adoption, then climate and environmental policy would not be at odds.

And they are correct. The only problem, it’s a useless statement. It’s akin to saying we could disband armies if we only learned to love thy neighbor. It’s a beautiful sentiment, but a profoundly naive one.

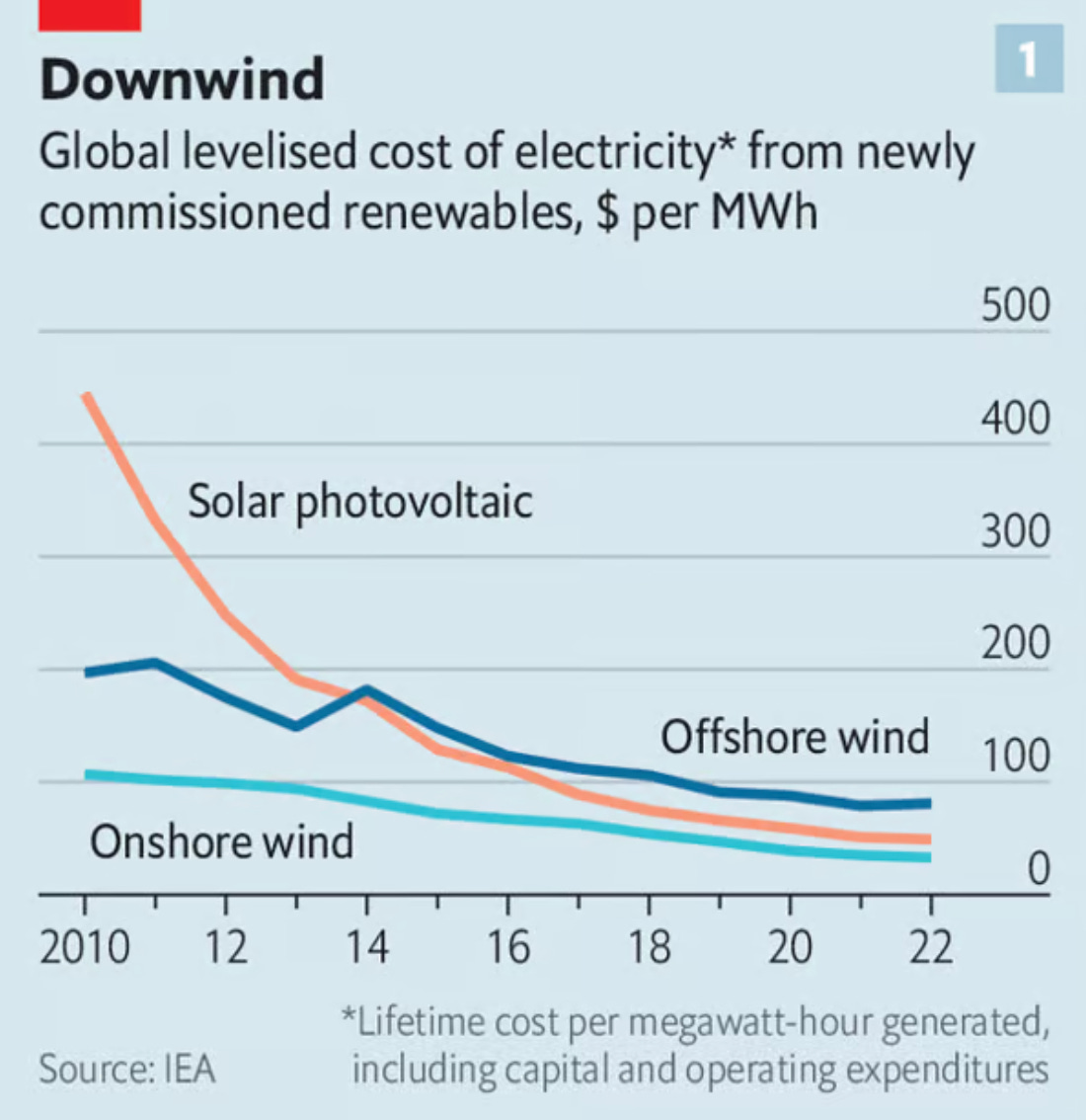

When it comes to power generation, the costs for wind, solar, and hydropower have indeed fallen. But storage solutions (large scale batteries) remain expensive and are not yet efficient enough to handle intermittency at the scale needed to maintain consistent energy supply.

Source

Heavy industries (e.g., steel, cement, and chemical production) rely on high-intensity energy from fossil fuels. Renewables and green hydrogen are not yet able to replace it at competitive costs or volumes.

For example, using hydrogen as a fuel source in cement production could increase costs by up to 214% at current hydrogen prices. You can read more about that in part II of my special III-part series on Saudi Arabia’s energy transition.

And as I wrote back in mid-September, the growing energy demands of AI will require consistent energy inputs. Fossil fuels and nuclear are able to achieve that far more efficiently than renewables are at this time.

Furthermore, the lack of infrastructure currently in place to facilitate the switch to renewables is an inhibiting factor. Estimates vary, but according to the National Renewable Energy Laboratory, it could cost between $440-$740 billion to decarbonize the US energy grid. And in my view, that’s optimistic.

But even if fiscal budgets were no issue, policymakers would return to the initial dilemma of choosing between climate and environmental policy. To avoid greenflation, more resources would need to be extracted to accommodate the surge in demand.

All of this is not meant to discourage innovation in renewables or energy transition efforts but to temper unhinged idealism with sober reality. The current conditions are not conducive for countries and companies to deploy both environmental and climate policy at scale without negative externalities.

The price of one is the other.