What to Expect From a Trump Presidency?

What should policymakers, investors, and businesses expect from a second Trump presidency?

Donald Trump was elected the 47th President of the United States last week, becoming the first since Grover Cleveland in 1892 to win a second, non-consecutive term after losing re-election.

With elections, it is easy to get caught up with hyperbolic alarmism emanating from the left and right about their opponents. Instead, this report will analyze Trump’s domestic and foreign policy frameworks and provide a sober assessment of its implications for the economy.

While the case for inflation is strong, the ripple effects of tariffs and the geopolitical climate may tame economic dynamism and price pressure. In that scenario, the US economy could experience moderate growth with limited inflationary pressure. There is precedent for it - his first term.

Fiscal Policy

Tariffs

Donald Trump’s proposed tariff policies for 2024 reflect his signature protectionist approach to trade, aiming to boost domestic manufacturing by imposing significant barriers to imports.

Key components include a baseline 10-20% tariff on all imports, with targeted tariffs reaching as high as 60% on Chinese goods to counter alleged unfair trade practices. But this is nothing new.

Back in May, Mr. Biden tweeted out: “I just imposed a series of tariffs on goods made in China: 25% on steel and aluminum, 50% on semiconductors, 100% on [electric vehicles], and 50% on solar panels. China is determined to dominate these industries. I'm determined to ensure America leads the world in them”.

When it comes to foreign policy vis-a-vis China, there is a secular orthodoxy between presidents and across the congressional aisle of taking China on more directly. Tariffs and export controls are in vogue.

For better or for worse.

Trump has specifically mentioned a 100% tariff on cars manufactured in Mexico. This is no accident: China has been setting up industrial hubs in other countries and using them as intermediaries to export to the U.S.

As I wrote in a report back in August:

“Although many nations will face economic challenges from global fragmentation, a select few are positioning themselves to benefit from the shifts spurred by the U.S.-China rivalry”. You can read the full article here.

Mexico is no different: Chinese automakers like BYD, Chery, and MG Motors are setting up facilities there, with a focus on EV production. These vehicles are aimed at both the Mexican and U.S. markets.

For instance, BYD is establishing a factory in Mexico as a hub for exporting affordable EVs to the U.S. market, leveraging trade agreements to circumvent tariffs imposed on Chinese exports.

By operating in Mexico, these companies avoid the high tariffs on Chinese goods imposed under Section 301 by the U.S., while meeting local assembly requirements that allow their products to qualify for lower tariffs or incentives like EV tax credits in the U.S

In 2018, the Trump administration launched a full-scale trade war with China, invoking Section 301 of the Trade Act of 1974 as the legal framework. This marked a pivotal shift in U.S. trade policy, moving from multilateral arbitration through institutions like the WTO to a more unilateral approach.

The use of Section 301 gave the U.S. the ability to address what it deemed unfair Chinese practices, bypassing lengthy global arbitration processes.

The administration imposed tariffs on $50 billion of Chinese imports in 2018, focusing on technology-heavy sectors like machinery and electronics. This initial wave escalated into a series of tariffs, eventually covering $360 billion worth of Chinese goods by the end of 2019.

It is likely he will employ similar measures and legal frameworks in his second term.

Tax Cuts

Trump intends to make the tax cuts under the 2017 Tax Cuts and Jobs Act (TCJA) permanent, including maintaining the top individual income tax rate at 37% (instead of reverting to the pre-TCJA rate of 39.6%).

He is also proposing on reducing the corporate tax rate further from the current 21% to 15%. In line with his platform, this would primarily apply specifically to companies that manufacture their products in the U.S.

Firms that outsource, offshore, or fail to comply with domestic production criteria would not qualify for this lower tax rate. Instead, they would remain subject to the standard corporate tax rate of 21% or face penalties e.g. tariffs.

He has also proposed restoring full "bonus depreciation" for business investments. This measure was originally introduced in the TCJA, which allowed businesses to immediately deduct 100% of the cost of eligible capital investments, such as equipment and machinery.

However, this provision began phasing out in 2023 and is scheduled to fully expire by 2027. Trump aims to reverse this phase-out and make the 100% deduction permanent.

Mass Deportations

Donald Trump's proposed mass deportation plan aims to remove millions of undocumented immigrants from the United States, marking a significant shift in immigration policy.

Legal scholars have pointed to Trump invoking the Alien Enemies Act of 1798, a law historically used during wartime to detain or deport nationals from enemy countries. Trump suggests applying this act to expedite the removal of individuals he deems threats to national security, such as members of foreign gangs like Venezuela's Tren de Aragua.

The plan involves mobilizing federal agencies, including Immigration and Customs Enforcement (ICE) and the Department of Homeland Security (DHS), to identify, detain, and deport undocumented individuals.

This would involve constructing additional detention centers or expanding existing ones to house individuals awaiting deportation. Trump also aims to expedite legal proceedings by increasing the number of immigration judges and reducing bureaucratic hurdles, thereby accelerating the removal process.

Deregulation

Trump pledges to cut 10 existing regulations for every new one, aiming to lower the operational costs for U.S. manufacturers. Other notable sectors and industries he is looking to deregulate include the following:

Environmental and energy policies would be overhauled to reduce barriers for industries such as oil, gas, and heavy manufacturing.

Easing capital requirements for banks, encouraging lending and investment. This would complement a rollback of antitrust measures, making it easier for companies to expand through mergers.

For technology, this would involve streamlining approval processes for broadband projects to accelerate infrastructure growth. This would accompany plans to dismantle AI-related safeguards.

Industrial Policy

Many of the policies outlined above would constitute a form of industrial policy. But separate measures that fall under the fiscal umbrella include Special Manufacturing Zones.

These would be federal zones with ultra-low taxes and reduced regulations would be established to attract investment in strategic sectors like semiconductors and green energy.

For supply chain security, Trump’s policy emphasizes bringing critical industries, like semiconductors and EVs, back to the U.S. or relocating them to allied countries like Mexico under the USMCA framework.

This is not dissimilar to Mr. Biden, and therefore a part of the continuation of the macro secular trend of prioritizing on-shoring, near-shoring, and friend-shoring among major global economies.

Economic Effects

Tariffs

The most monitored economic policy of Trump’s are tariffs. The theory goes that exported goods entering the US will be tariffed, importers will raise their prices, and domestic goods will be comparatively cheaper, and that in turn will fuel domestic growth.

The only small problem is that’s not how it works in practice.

When Trump imposed tariffs on Chinese goods during his first term, many consumers did not switch to domestic options. This is because in most cases, domestic goods were still more expensive or less readily available than imported alternatives.

Domestic manufacturers often face higher labor, regulatory, and operational costs compared to foreign producers, particularly in countries like China or Vietnam. Morally-laudable regulations do have a cost, and it’s baked into the goods we consume.

Even with tariffs adding 10-25% to the price of imports, these cost advantages often meant that imported goods remained cheaper than domestically produced alternatives.

For example:

Washing Machines

Imported Brands (Samsung, LG):

Pre-Tariff Price (2017): Approximately $900.

Post-Tariff Price (2018, with 20% Tariff): Increased to around $1,000.

Domestic Brand (Whirlpool):

Pre-Tariff Price (2017): Approximately $1,000.

Post-Tariff Price (2018): Rose to about $1,100.

Automobiles

Imported Models (Toyota Camry, Honda Accord):

Pre-Tariff Price (2018): Approximately $25,000.

Post-Tariff Price (2019, with proposed 25% Tariff): Increased to around $31,250.

Domestic Models (Ford Fusion, Chevrolet Malibu):

Pre-Tariff Price (2018): Approximately $24,000.

Post-Tariff Price (2019): Increased to about $25,500 due to higher costs of imported components.

Footwear

Imported Brands (Nike, Adidas):

Pre-Tariff Price (2018): Average athletic shoes priced at $60.

Post-Tariff Price (2019, with 10% Tariff): Rose to about $66.

Domestic Brand (New Balance):

Pre-Tariff Price (2018): Approximately $100.

Post-Tariff Price (2019): Increased to around $110.

To avoid data-exhaustion, I will stop the examples here, but this applies to many other goods for household items that saw their prices rise.

In electronics, most components and assembly processes occur in Asia, making it nearly impossible for domestic producers to fill the gap quickly. Biden’s CHIPS Act was in part a response to remedy this post-globalization ailment.

The takeaway is prices rose. But it also had broader macroeconomic effects: the tariffs imposed between 2018 and 2019 contributed an estimated 0.3-0.5 percentage points to core inflation annually.

A Federal Reserve study found that U.S. consumers bore 92% of the tariff burden, as importers passed on the higher costs to retail prices.

The Congressional Budget Office (CBO) estimated that Trump’s tariffs reduced U.S. GDP by 0.1% annually between 2018 and 2019, equating to approximately $20 billion per year. This was driven by higher costs for businesses and reduced export opportunities due to retaliatory tariffs.

The steel and aluminum sectors, protected by 25% and 10% tariffs, saw production increases of 5% and 2%, respectively. However, downstream industries like automotive manufacturing faced higher input costs, offsetting gains in raw material production.

Tariffs on imports generated approximately $79 billion in tax revenues in 2020, according to the U.S. Treasury Department. This marked a substantial increase from $36 billion in 2017 before the tariffs. But while tariffs provided a direct revenue stream, they also acted as a tax on consumption.

The Tax Foundation estimated that higher import prices due to tariffs effectively offset 20-25% of the benefits from the 2017 Tax Cuts and Jobs Act (TCJA) for middle-income households.

But the tariffs are not guaranteed to reignite inflation and undo the effects of the Fed’s monetary tightening. During Trump’s first term, global trade growth slowed to 0.8% in 2019, down from 4.6% in 2017 before the trade war began.

As the trade war escalated in 2019, the global economic slowdown and rising uncertainty began to weigh on U.S. growth. Business investment contracted, and manufacturing entered a recessionary phase.

In response, the Fed cut interest rates three times in 2019, lowering the federal funds rate to a range of 1.50-1.75% by the end of the year. These cuts were intended to counteract the economic drag from the trade war and stabilize financial markets.

For historical context, before the trade war, the Federal Reserve pursued a hawkish monetary policy, raising interest rates four times in 2018 to a range of 2.25-2.50%. This reflected strong economic growth, unemployment at 50-year lows, and inflation nearing the Fed's 2% target.

In other words, the deflationary ripple effects of tariffs may counter the inflationary aspects of that policy.

Tax Cuts

The TCJA’s initial impact was striking. Real GDP growth in Q1 2018 reached 2.2% annualized, up slightly from 2.0% in Q4 2017, reflecting early increases in consumer spending and business investment.

By Q2 2018, growth surged to 4.2%, the highest quarterly rate since 2014, as businesses capitalized on new provisions like reduced corporate tax rates and full expensing for capital expenditures.

Momentum continued into Q3 2018, with GDP growing at 3.5%, supported by consumer expenditure and inventory investments. However, by Q4 2018, growth slowed to 2.5%, signaling a return to more sustainable levels after the initial surge.

The economy expanded by 2.9% in 2018, matching the peak of 2015 and representing one of the strongest annual performances in recent years. But by 2019, the effects of the tax cuts began to wane, and growth slowed to 2.3%.

While the TCJA injected significant fiscal stimulus into the economy, inflation remained subdued. The Personal Consumption Expenditures (PCE) price index, the Federal Reserve’s preferred inflation metric, rose to 2.0% by May 2018, hitting the Fed’s target.

Despite higher consumer demand and business spending, inflationary pressures did not accelerate as anticipated. By late 2018 and throughout 2019, inflation weakened, with the PCE index fluctuating between 1.5% and 1.8%.

This was partly due to global disinflationary trends and supply chain adjustments tied to trade tensions. Considering Mr. Trump’s policy proposals, it is not unrealistic to price in another similar dynamic.

Mass Deportations

This remains one of the biggest question marks to the extent that the logistics, scale, and legal feasibility of the operation has not been completely mapped out. Trump said up to 20 million illegal immigrants may be forced out of the country.

Trump’s team is reportedly exploring the option of declaring a national emergency at the southern border immediately upon his return to office. This declaration would potentially allow the government to redirect Pentagon funds for building additional sections of the border wall.

It could also facilitate the use of military bases to house detainees and military aircraft to speed up deportation efforts. However, these actions are expected to face significant legal scrutiny, as the scope of such a declaration is highly contested.

As for the economic effects, depending on the magnitude and speed, it could cause a dramatic spike in inflation for staple goods. Illegal immigrants in the US constitute approximately:

50% of all agriculture workers

15% of all construction workers

8-10% of all hospitality and services workers

It would therefore not be surprising if a sudden disappearance of a substantial portion of the workforce in these industries would turbo-charge inflation. This policy poses the largest macroeconomic risk.

The only scenario in which inflation would not remain painfully high is if the deflationary contraction caused by removing undocumented immigrants outweighed the inflationary pressures from labor shortages. But that is not likely.

Deregulation

The White House Council of Economic Advisers (CEA) estimated that deregulation contributed approximately 0.8% to GDP growth from 2017 to 2019. This equates to roughly $200 billion in economic output over three years.

The American Action Forum (AAF) reported that regulatory rollbacks reduced compliance costs by $220 billion during Trump’s first term. Lower compliance costs incentivized business investment, particularly in industries such as manufacturing, energy, and construction.

For example, removing regulations on emissions standards and environmental reviews for infrastructure projects accelerated construction timelines, contributing to a 2.4% increase in business investment in 2018.

Deregulation’s growth effects were largely non-inflationary, as they improved supply-side efficiencies. Inflation remained subdued during this period, with the Federal Reserve’s PCE price index averaging 2.0% in 2018 and 1.6% in 2019.

This indicates that deregulation helped expand supply, offsetting inflationary pressures from fiscal stimulus and rising consumer demand

Industrial Policy

The overall impact on inflation from Trump’s Special Manufacturing Zones would depend on the interplay between short-term costs and long-term supply-side benefits.

In the short term, the zones would likely exert inflationary pressure. This would stem from increased government spending on infrastructure and subsidies, heightened demand for labor in construction and manufacturing, and potential input shortages as production ramps up.

Over the long term, however, the effects could become deflationary. By increasing domestic production capacity, the zones would expand supply, reduce reliance on volatile foreign trade, and enhance productivity through localized manufacturing.

This shift could stabilize prices and counteract inflationary risks over time, provided the initial investment yields sustained economic efficiency. Like Biden’s CHIPS Act, the effects are localized and do not significantly impact the broader national economy. This would likely be the same.

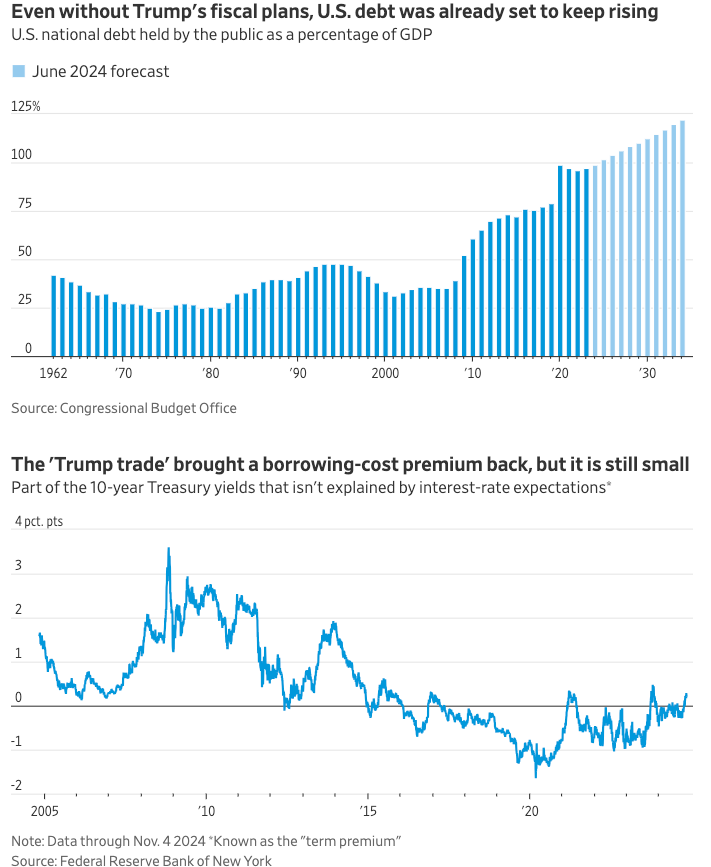

Federal Deficit

The Committee for a Responsible Federal Budget estimates that Trump’s proposed policies could increase the national debt by $1.6 trillion to $15.6 trillion over the decade from 2026 to 2035. The wide range reflects uncertainties around implementation and the economic response to his fiscal agenda.

Following Trump’s election victory, the dollar surged alongside equity indices and bond yields. The Greenback rose alongside government debt borrowing costs on the expectations that Trump’s policies would be inflationary and would therefore prompt the Fed to raise interest rates.

Trump’s proposed policies, while likely to expand the federal deficit, benefit from the United States’ unique position as the issuer of the world’s primary reserve currency.

The U.S. dollar’s status as a reserve currency provides significant financial flexibility, allowing the government to borrow at lower costs compared to nations without this privilege. This is because global demand for dollars, driven by its use in international trade and as a safe-haven asset, ensures consistent liquidity in U.S. Treasury markets, even amid rising debt levels.

The long-term worries and risks associated with a deep federal deficit are not unique to Trump. Those concerns were articulated about Kamala’s plans as well, and has pre-dated this presidential election by decades. It’s therefore not necessary to expand on those long-term risks in this report.

What is clear is that Mr. Trump’s approach to defying political orthodoxy with sweeping economic reforms will have profound consequences. What remains opaque is whether they will usher in economic pain, prosperity, or a purgatorial blend of the two.