Mining Stocks May Surge on Global Energy Transition. But There's a Catch

The move to green tech will mean demand for transition metals will surge, and mining company shares may catch a multi-year tailwind. But it's not so simple.

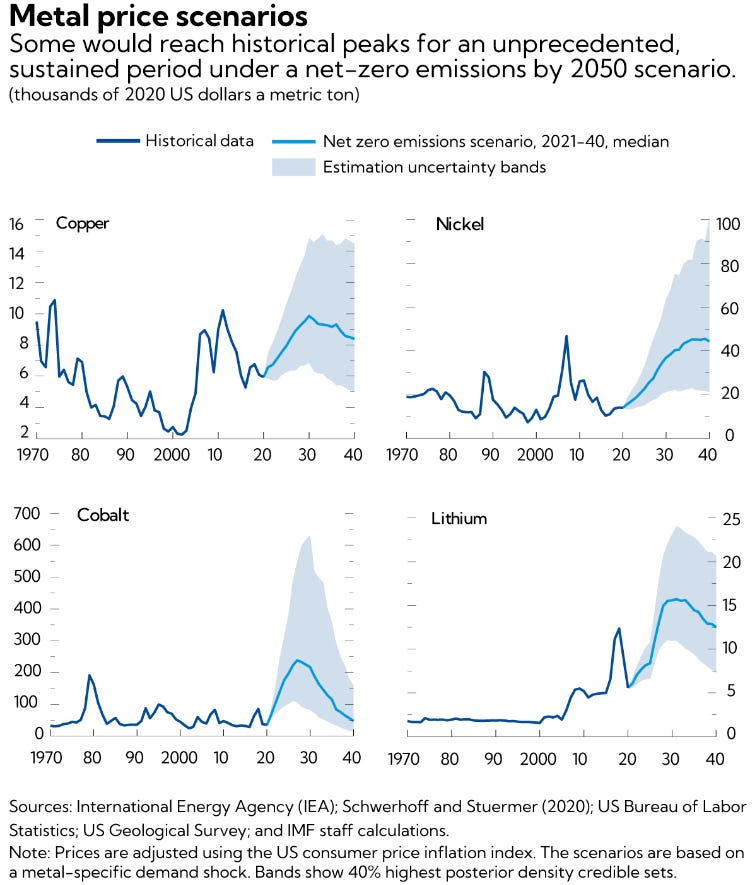

The Risks of Greenflation

The push to move away from fossil fuels and instead towards carbon neutral alternatives means demand for so-called transition metals will surge. The IMF estimates that copper, nickel, cobalt, and lithium will be most impacted by the global energy transition.

In a scenario where renewables are the primary source of energy in 2030, they forecast the prices for nickel, cobalt, and lithium to rise by several hundred percent from 2020 levels, and for copper by approximately 60%

Source: IMF

An electric car requires five times more of these metals than a conventional car, and when it is plugged into the grid for recharging, that grid itself is mostly powered by hydrocarbons. According to Wood Mackenzie, transforming just the US power grid alone would cost $4.1 trillion over 10 years.

In other words, the energy transition is resource-demanding, and states will still require fossil fuels to function. If major economies like the US or China don’t use a blend of hydrocarbons and green alternatives, it elevates the risk of so-called greenflation: a rise in the prices of resources resulting from the energy transition.

Why Mining Companies May Benefit

Results show that the supply of all metals, except lithium, are relatively inelastic over the short term. A surge in what would be a semi-structural increase in demand without a proportional increase in supply would accelerate the prices of these transition metals. This in large part has to do with the nature of the mining industry.

The operationalization of mines - i.e. construction, acquiring permits, etc - has increased from five to 10 years as a result of extensive environmental and social impact regulations.

Publicly-traded mining companies in particular are under pressure from shareholders to adhere to ESG metrics while maintaining their operations. However, the increased costs from incorporating environmental, social, and governance factors means production and expansion will be costlier and slower as a result.

The gap between the surge in demand but lagging supply will likely translate to higher commodity prices that mining companies can add to their bottom line. The bulk of this greenflationary trend will largely be a multi-faceted supply problem.

There is also a deep and narrow geographic concentration of these strategic transition metals/resources in regions with a history of political instability.

Countries with large deposits of key inputs as a % of world total:

~70% Cobalt ➡️ DRC

~30% Lithium ➡️ Chile

~27% Graphite ➡️ Turkey

~75% Manganese ➡️ South Africa

Political stability ranked by each country on a scale of -2.5 (weak) to 2.5 (strong):

DRC: -1.61

Chile: 0.06

Turkey: -1.1

South Africa: -0.71

All taken into account, the lag time between supply meeting semi-structural demand will create an upward price gap for these transition metals. Mining companies specializing in the extraction and processing of these strategic resources may therefore see wider profit margins and higher share prices.

However, no investment is without risk, and there is always a price to pay.

All That Glitters…

Mining firms carry a plethora of risks in an industry that is facing increased scrutiny and asymmetric risks in the current geopolitical environment. One major risk to consider with mining companies is corruption.

The OECD Foreign Bribery Report estimates that 20% of foreign bribery occurs in the extractives industry i.e. mining support services, quarrying, etc. Glencore, the world’s largest mining company in the world by revenue, has incurred over $1 billion in fines between November 2022 and February 2023 alone.

While its revenue in 2022 was $256 billion, profits were by comparison a meager $17.3 billion. *To settle their fines, firms will use existing financial resources e.g. cash reserves, operating income, or other sources of funds. While the payment of fines reduces their available cash or financial resources, it does not directly reduce the firm’s revenue. Having said that, it can affect the company's profitability for the period in which the fines are incurred.

Digression aside, another major risk is geopolitical. Countries with poor governance, high inequality, and corruption are vulnerable to domestic social unrest. These include riots, coups - as we are seeing in Africa - and other operation-disrupting risks.

Nationalization of foreign industries - particularly those that are responsible for a large portion of the country’s jobs and national income - is known to be a tactic employed by military junta.

Another risk to consider is volatility. Commodities are notorious for price oscillations and can therefore have severe implications for profit margins, revenue, and project viability. With the rate of cost-saving technological innovation and surging demand for key resources, the potential for volatility and risk widens at a commensurate rate.

And a final risk to consider is regulation. The mining industry has come under increased scrutiny, particularly from a rising tide of higher ESG thresholds. Despite the leverage mining companies wield in countries that depend on their investments, the industry as a whole is subject to strict regulatory oversight.

Despite some bright prospects, I would argue that geopolitical and regulatory complications will continue to remain headline risks for mining companies.

*None of the above constitutes financial advice.